Berita Terkait

- Anggaran DPR RI Tahun 2016-2018

- Kehadiran Anggota DPR Pada Masa Sidang Ke-2 Tahun 2017-2018

- Review Kinerja DPR-RI Masa Sidang ke-2 Tahun 2017-2018

- Fokus DPR Masa Sidang ke-3 Thn 2017-2018

- Konsentrasi DPR Terhadap Fungsinya Pada Masa Sidang ke - 3 Tahun 2017 – 2018

- Kehadiran Anggota DPR RI Masa Sidang ke-3 Tahun 2017-2018

- Review Kinerja Masa Sidang Ke-3 Tahun 2017-2018

- Konsentrasi DPR Terhadap Fungsinya Pada Masa Sidang ke - 4 Tahun 2017– 2018

- Peristiwa Menarik Masa Sidang ke-4 Tahun 2017-2018 (Bidang Legislasi)

- Peristiwa Menarik Masa Sidang ke-4 Tahun 2017-2018 (Bidang Pengawasan)

- Peristiwa Menarik Masa Sidang ke-4 Tahun 2017-2018 (Bidang Keuangan, Lainnya)

- Review Kinerja DPR-RI Masa Sidang ke-4 Tahun 2017-2018

- (Tempo.co) Kasus Patrialis Akbar, KPPU: UU Peternakan Sarat Kepentingan

- (Tempo.co) Ini Proyek-proyek yang Disepakati Jokowi-PM Shinzo Abe

- (Tempo.co) RUU Pemilu, Ambang Batas Capres Dinilai Inkonstitusional

- (Media Indonesia) Peniadaan Ambang Batas Paling Adil

- (DetikNews) Besok Dirjen Pajak Panggil Google

- (Tempo.co) Aturan Komite Sekolah, Menteri Pendidikan: Bukan Mewajibkan Pungutan

- (Rakyat Merdeka) DPR BOLEH INTERVENSI KASUS HUKUM

- (Aktual.com) Sodorkan 4.000 Pulau ke Asing, Kenapa Pemerintah Tidak Menjaga Kedaulatan NKRI?

- (RimaNews) Pimpinan MPR dan DPR akan bertambah dua orang

- (Warta Ekonomi) Jonan Usulkan Kepada Kemenkeu Bea Ekspor Konsentrat 10 Persen

- (Tempo.co) Eko Patrio Dipanggil Polisi, Sebut Bom Panci Pengalihan Isu?

- (TigaPilarNews) DPR Harap Pemerintah Ajukan Banyak Obyek Baru untuk Cukai

- (Tempo.co) Menteri Nasir: Jumlah Jurnal Ilmiah Internasional Kita Meningkat

Kategori Berita

- News

- RUU Pilkada 2014

- MPR

- FollowDPR

- AirAsia QZ8501

- BBM & ESDM

- Polri-KPK

- APBN

- Freeport

- Prolegnas

- Konflik Golkar Kubu Ical-Agung Laksono

- ISIS

- Rangkuman

- TVRI-RRI

- RUU Tembakau

- PSSI

- Luar Negeri

- Olah Raga

- Keuangan & Perbankan

- Sosial

- Teknologi

- Desa

- Otonomi Daerah

- Paripurna

- Kode Etik & Kehormatan

- Budaya Film Seni

- BUMN

- Pendidikan

- Hukum

- Kesehatan

- RUU Larangan Minuman Beralkohol

- Pilkada Serentak

- Lingkungan Hidup

- Pangan

- Infrastruktur

- Kehutanan

- Pemerintah

- Ekonomi

- Pertanian & Perkebunan

- Transportasi & Perhubungan

- Pariwisata

- Agraria & Tata Ruang

- Reformasi Birokrasi

- RUU Prolegnas Prioritas 2015

- Tenaga Kerja

- Perikanan & Kelautan

- Investasi

- Pertahanan & Ketahanan

- Intelijen

- Komunikasi & Informatika

- Kepemiluan

- Kepolisian & Keamanan

- Kejaksaan & Pengadilan

- Pekerjaan Umum

- Perumahan Rakyat

- Meteorologi

- Perdagangan

- Perindustrian & Standarisasi Nasional

- Koperasi & UKM

- Agama

- Pemberdayaan Perempuan & Perlindungan Anak

- Kependudukan & Demografi

- Ekonomi Kreatif

- Perpustakaan

- Kinerja DPR

- Infografis

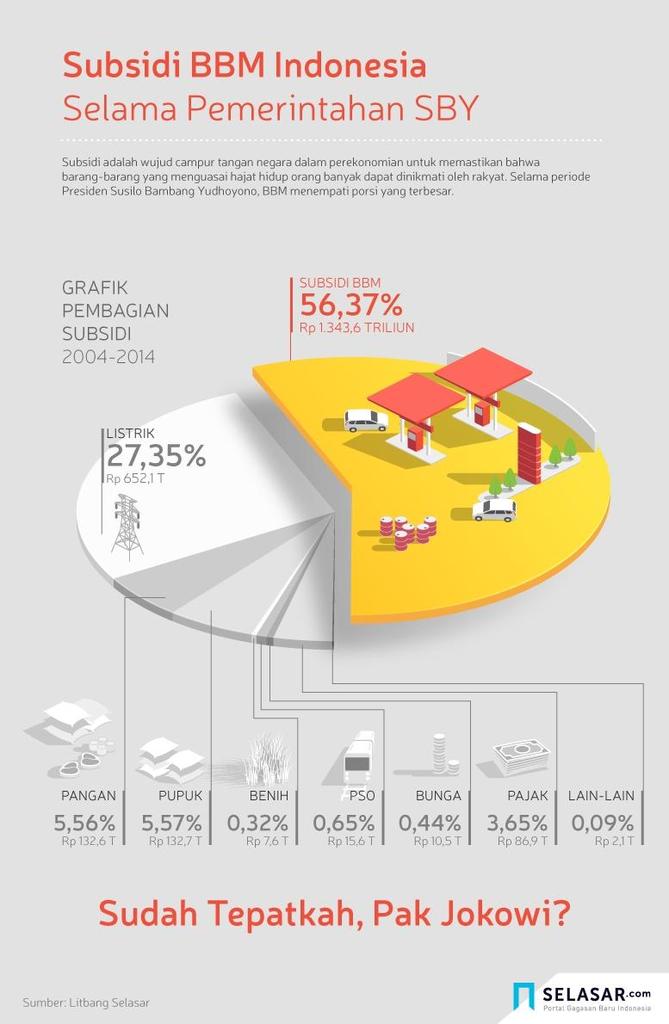

(DBS Insight) Indonesia Subsidy Cut Crucial for Current Account

In spite of the decline in global oil prices, a cut in Indonesian fuel subsidies is still crucial in order to narrow the country’s current account deficit.

On his current international trip, Indonesian President Joko Widodo will be making stops at the APEC, Asean and G-20 summits. Plenty of focus will be on the bilateral talks with China, various meetings with global business leaders as well as his push for maritime infrastructure development in Indonesia.

Still, the most important policy for the markets is closer to home, that of the planned fuel price hike. This policy move is seen to be a yardstick of the government’s commitment to tough reforms. Expectations for an aggressive 45% fuel price hike had built up ahead of the presidential inauguration last month. Hence, it is no surprise that markets have been somewhat disappointed that no move has been announced as yet.

Several local media outlets have suggested that the president may finally implement the fuel price hike upon his return to Jakarta next week. Yet, some now question the need to raise fuel prices, given the recent easing in the global crude oil price.

Lower global crude oil prices mean a lower fuel subsidy bill, a positive for the budget outlook. But it does not necessarily mean that the government should not alter its subsidised fuel price. After all, subsidised fuel consumption has surpassed the budgeted amount in recent years, which means that the actual fuel subsidy bill could theoretically end up as high despite falling global crude oil prices.

Furthermore, the current subsidised fuel price is still some 40% lower than the non-subsidised option. Raising the subsidised fuel price by 30%, for example, will only narrow this gap by about half. And the potential budget savings of about US$10-US$12 billion per year can be channelled into expenditure with higher multiplier effects, such as rural area infrastructure development.

More importantly, the fuel price hike is also crucial to help narrow the current account deficit. In volume terms, there has been a widening gap between exports and imports of petroleum (and its products) in the past two years. This is a real concern, especially noting that higher domestic production of oil, both crude and refined, will take time to bring about. Based on our current assumptions, a 30% fuel price hike will help to bring the current account deficit to about 2.7% of GDP in 2015 (projected at 3.0% of GDP in 2014). In the case of the 45% fuel price hike, the current account deficit is likely to be around 2.5% of GDP.